Bajaj Auto’s Growth Could Accelerate. Read Details Here

It’s a company that represented the aspirations of the rising middle class of India for decades. Bajaj Auto provides mobility to families, and also represents the ‘can do’ spirit of consumers.

And with the economy slowly reemerging from the twin shocks of Covid and rising fuel prices related to the Russia-Ukraine war, investors have been bullish on this auto stock.

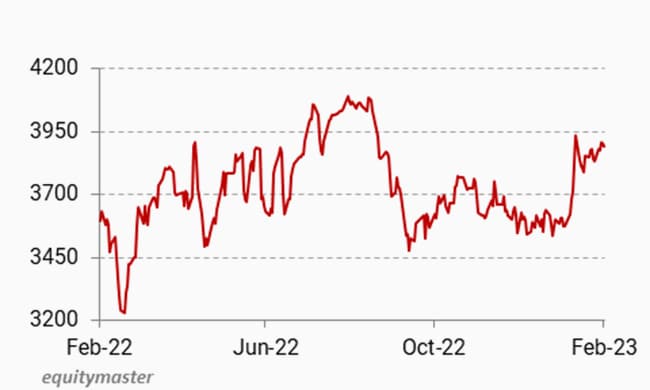

No surprise, that Bajaj Auto ended last week Friday’s trade at Rs 3,894, not too far from its 52-week high of Rs 4,130 touched on 1 September 2022.

Bajaj Auto Share Price – 1 Year Performance

Data Source: Ace Equity

This bullish sentiment comes at a time when the key operational performance of Bajaj Auto is sluggish.

For instance, total vehicle sales (two-wheelers and commercial vehicles) of Bajaj Auto declined 21% year-on-year (YoY) to 285,995 units in January 2023, and that was largely due to a 46% fall in two-wheeler exports to 100,679 units in the month under review.

Also, during April – January of FY23, total vehicle sales of the Pune-based company declined 9% YoY to 3,353,929 units, given weak demand conditions in overseas markets for its two-wheelers.

Meanwhile, nearest rival Hero MotoCorp saw its sales decline 6.2% YoY to 356,690 units in January 2023.

However, during April till January of the current financial year, total vehicle sales of this New-Delhi based company grew 6.7% to 4,414,744 units.

Smaller rival, TVS Motor Company reported a sales growth of 3% YoY to 275,115 units in January 2023.

Managing costs

Bajaj Auto had the highest operating profit margins in the December 2022 quarter in the two-wheeler segment.

The company’s operating margins grew 370 basis points YoY to 21.9% in the quarter under review. Tight check on costs helped the Pune-based company grow its standalone net profit 22.8% YoY to Rs 14.9 billion (bn) while revenue from operations grew just 3.3%.

In the case of Hero MotoCorp, its operating profit margins were broadly flat at 13.8% on a YoY basis in the third quarter of current financial year.

Similarly, TVS Motor’s operating profit margins were broadly flat at 10.1% on a YoY basis in the December 2022 quarter.

Investor sentiment

Investors are hoping that the government would shortly accept the two-wheeler industry demand for reducing GST from 28% to 18%.

Also, signs of easing in raw material prices have kept investor sentiment bullish for this sector.

As a result, TVS Motor ended Friday’s trade at Rs 1,104 and not too far from its 52-week high of Rs 1,177 that was reached on 19 October 2022.

Hero MotoCorp ended Friday’s trade at Rs 2,534 vis-à-vis its 52-week high of Rs 2,939 that was reached on 18 August 2022.

Valuations

Bajaj Auto trades at 18.5 times estimated FY23 earnings and 16 times estimated FY24 earnings.

Meanwhile, Hero MotoCorp trades at 18 times estimated March 2023 earnings and 17 times estimated March 2024 earnings.

And TVS Motor trades at 36 times estimated March 2023 earnings and 29 times estimated March 2024 earnings.

Bajaj Auto trades at a price to earnings (PE) multiple broadly in tune with its nearest rival Hero MotoCorp.

However, until the sales momentum in overseas markets picks up, growth opportunities appear limited for Bajaj Auto in the near term.

Investors could instead consider other two-wheeler stocks with a strong focus on the domestic market.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com

(Except for the headline, this story has not been edited by NDTV staff and is published from a syndicated feed.)